Energy Musings - September 3, 2024

The second quarter financial results of German industrial company ThyssenKrupp highlighted the problems local manufacturers are having because of energy costs and faultering demand.

Germany And Its Industries Struggle

The Wall Street Journal reported on the latest financial results of ThyssenKrupp AG a couple of weeks ago. The company describes itself as “an international industrial and technology company” but its roots and focus is on Germany. In 2023, in response to the continuing economic turmoil of 2020-2023, initially driven by the pandemic and then the invasion of Ukraine by Russia, ThyssenKrupp began a corporate restructuring to improve its operating efficiencies and boost profits. The company operates in five sectors: Automotive Technology, Decarbon Technologies, Materials Services, Steel Europe, and Marine Systems.

For the company’s third quarter ending June 30, it reported a net loss of €54 ($59.4) million, compared to a profit of €83 ($91.3) million a year ago. Sales for the quarter fell 6% year on year. Noteworthy was for the third time this year, the company’s management cut its profit forecast. They had previously reduced their outlook in February and again in May as continued market weakness and lower sales plagued their results. ThyssenKrupp now expects a net loss in the mid-to-high three-digit-million-euro range for its fiscal year ending in September. Previously, the company had expected the fiscal-year net loss to be in the low three-digit-million-euro range. Following the results, the share price of ThyssenKrupp fell 6%.

One restructuring move the company has undertaken is the complex carve-out of its steel unit. The first step was to sell a 20% interest to Czech billionaire Daniel Kretinsky’s EP Corporate Group. The challenge is that the steel unit’s earnings in the third quarter were nearly cut in half due to price and demand pressures. The lower prices and volumes were especially noted in the automotive sector where Germany’s and Europe’s auto manufacturers suffer from reduced demand and increased competition from Chinese imports. ThyssenKrupp’s material services unit also suffered from lower prices for finished steel products.

These market and cost pressures come at a difficult time as the company is negotiating with EP Corporate Group to sell another 30% of its steel unit to create a joint venture business. ThyssenKrupp also intends to exit Huettenwerke Krupp Mannesmann, its steel venture which includes Germany’s Salzgitter and France’s Vallourec. The plan following this separation is for a standalone European steel business. That would allow management to reduce its crude steel manufacturing capacity.

ThyssenKrupp is also exploring the realignment of its automotive body solutions unit. It plans to cut jobs in its German operations while seeking to expand capacities at international facilities. This planned restructuring, expected to be implemented by the end of fiscal 2025, is a response to the deteriorating European automobile market. European auto manufacturers have seen their global competitiveness eroded by high electricity costs and increased Chinese automobile market share gains.

As part of its restructuring efforts, the company has halted its automation engineering business divestment effort. It is now exploring options for its powertrain business in Bremen, Germany.

ThyssenKrupp’s steel business market problems are also experienced by its German peers. Additionally, the company is wrestling with the green energy transformation mandated by government climate policies. The policies promoting this transformation were supposed to have ushered in a brighter future for the industry. But it has not arrived and may never arrive.

In response to this transformation mandate, ThyssenKrupp Steel is switching from coal to renewable hydrogen and it is proving to be very costly. Why? Because the cost of green energy inflates the price of steel which will make the industry non-competitive. Let’s look at the numbers.

Converting a steel manufacturing plant will cost maybe $800 million for a 2 million metric ton direction reduction (DRI) plant according to an analysis by the Energy Transition Commission. That translates into $43 per ton of steel produced. The problem is the cost of the green hydrogen required to power the DRI plant.

ThyssenKrupp is working to find out what the cost of green hydrogen will be. Remember, green hydrogen is made using renewable energy to split water into its parts and capture the hydrogen molecules. The company issued a tender for green hydrogen supply. However, a ballpark estimate for the energy needed to make one ton of steel is $450. When you add in the cost of the ore, labor, and everything else required by the plant – an estimated $380 per ton – plus an amortization charge for the capital investment of the plant, you get a steel cost of $870 per ton.

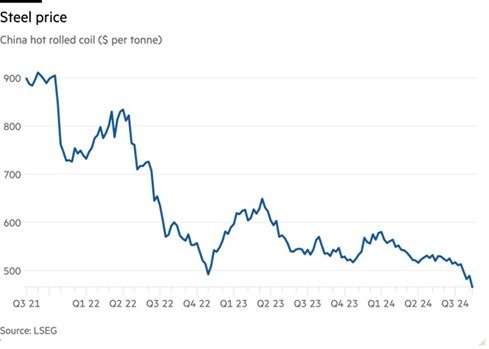

The German government has awarded subsidies to ThyssenKrupp for capital and operating expenses in this hydrogen transition which is designed to help the company compete against the cost of making dirty steel. The chart shows the price history for China’s hot rolled coil steel from 3Q 2021 to now. The price has dropped from $900 per ton to under $500. A steel analyst with investment bank Barclays estimates the current cost to make dirty steel in Europe is $580 per ton, which he estimates will rise to $730/ton by 2035. That reflects inflation in operating expenses and rising carbon prices. On the other hand, expectations are that the price of hydrogen will decline as the capacity to produce the fuel grows. Therefore, the gap between Europe’s dirty steel cost and the estimated cost for hydrogen-produced steel should shrink.

China’s low steel price is undercutting European steel which is wrestling with converting production to carbon-free fuel sources.

Unfortunately, that may not be the proper comparison. Rather, the cost of Europe’s hydrogen-produced steel should be compared to the cost of producing steel from hydrogen in areas with cheap renewable energy. A new study by the McKinsey Global Institute examines the challenges of the energy transition. The study, “The hard stuff: Navigating the physical realities of the energy transition” explores the 25 physical challenges the authors have identified that must be in place for carbon emissions to be eliminated by 2050. They state that only 10% of the progress has been achieved.

Hydrogen issues are physical challenges 20 and 21 identified in the study. Harnessing hydrogen and then scaling its infrastructure represent those challenges. In the Executive Summary of the report, the authors highlighted the hydrogen challenges. “First, the hydrogen molecule goes through many steps and therefore energy losses before it can be used; these would need to be minimized and weighed against its advantageous properties. Second, hydrogen production and infrastructure would need to expand hugely. Few large-scale low-emissions hydrogen projects are currently operational.”

Because producing hydrogen requires large volumes of water, Germany would need to source its hydrogen offshore. The hydrogen must be transported from its production site to the German steel plants. The small size of the hydrogen molecule creates physical challenges for shipping the gas through pipelines. These challenges will elevate the cost of hydrogen.

Forcing the German steel business to give up using neighboring coal resources puts it at a competitive disadvantage to those foreign steel producers using renewable energy. That is because the cost of moving steel across the water is and will likely always be cheaper than what it costs to ship the hydrogen used in the German effort.

Germany’s steel industry problems are caused by the country’s weak economy which is depressing its automobile and industrial industries. Those industries are suffering from the high cost of energy in the country. The latest economic shows German exports fell in June. The government attributes half of the decline to the competitive pressures hurting Germany’s key manufacturing industries. Cheaper suppliers of competitive products are eroding Germany’s industrial might, the driver of its economy for decades.

The weak economic outlook is reflected in revised estimates for Germany’s Gross Domestic Product growth. An article by Bloomberg reports that the government’s economic estimate for 2024 GDP growth has been cut to 0.1% from 0.2%. The reduction was partially attributed to the surprising second-quarter contraction. The official 2025 GDP growth estimate has also been trimmed by 0.1 percentage points to 1.1%.

Other economic estimates confirm the weak economy. The European Commission also has Germany’s GDP growth at 0.1% for 2024. The International Monetary Fund began the year projecting growth of 0.9% but the country’s budget crisis, the farmer protests, and the second quarter contraction have forced the agency to reduce its growth estimate to 0.2%. An example of how surprised economic forecasters were was the 2Q 2024 estimate from economic consultant ifo. It estimated the second quarter should show 0.3% growth only to decline by 0.1%.

The weak German economy has been a part of the legacy of Chancellor Olaf Schulz’s term in office. Since he was elected to head the government, Germany has experienced growth in fewer than half the ten quarters he has served. With an election in 2025, Schulz needs to work to boost the German economy if he wants his party to win and his leadership to continue. Watch for changes to Germany’s energy, climate, and geopolitical policies if things economically do not improve soon.