Energy Musings - September 1, 2023

Three stories in this edition. NJ's push to ban ICE vehicle sales is about free federal money; GOM wind lease sale bust as Orsted takes $2.3 billion impairment; Energy stocks and prices do well

NJ Calls It “Choice” But It Is Really About “Free Money”

New Jersey Governor Phil Murphy is a big green energy promoter. As the Wall Street Journal pointed out in an editorial, he wants to force residents to buy electric vehicles (EV) to save the planet. He has pushed the state to adopt California’s ban on the sale of new internal combustion engine (ICE) vehicles by 2035, barely over a decade from now. Murphy has not only championed EVs, but he also led the charge to give the state’s share of federal tax revenues from offshore wind destined for residents’ pocketbooks back to Ørsted, the Danish developer of the Ocean Wind project which has become a lightning rod of political outrage.

By wanting to burnish his green credentials, Murphy pushed to have New Jersey, one of the 17 states that routinely follow California’s auto standards, join the dozen states that have also signed onto the ban on ICE vehicle sales. Murphy is selling his proposal as expanding the vehicle choice options for residents while disguising the reality that their ability to purchase a new ICE vehicle is going to be restricted as the state heads toward the 2035 ban.

The impact of the ICE vehicle sale restriction was outlined in a letter from auto manufacturer Stellantis to its dealers. The Wall Street Journal quoted: “In some circumstances, we may be compelled to allocate more electrified powertrain vehicles to California states.” By jumping on the gas-engine car sales ban, New Jersey will become one of those “California states.” The question is whether there will be sufficient EVs to meet the California states’ bans.

We have argued for years when gas-engine car bans first emerged in Europe that ICE vehicle buyers will need to get in line at the start of the selling season because late-arriving buyers may only find EVs left on dealers’ lots. Ah, but New Jersey’s Kate Klinger, Director of the Governor’s Office of Climate Action and Green Economy, has other options for car buyers – used cars.

As she told ROI-NJ in an interview: “’There’s a lot of misinformation about what this order does,’ she said. ‘It requires that new vehicle sales in the state are zero emission by 2035. More than 50% of vehicles that are sold in the state are used. And there is absolutely no change to the used vehicle market.’”

She went on to say, “’You could get a hybrid, you could get an EV, you could go to another state that has not adopted (this regulation),’ she said. ‘New ICE vehicles purchased in New Jersey — I’ll give you that, that would not happen. But choices abound.’”

Going to a neighboring state only means more buyers for a shrinking pool of ICE vehicles because of the U.S. Environmental Protection Agency’s revised fleet fuel-efficiency standards that effectively will ban ICE vehicles, or impose huge fines on automakers who fail to meet the tightened standards.

An alternative Ms. Klinger failed to mention was making New Jersey’s highways look like Cuba’s roads, where classic vehicles are continually repaired to keep them running since buying new and used cars is limited. After the 1960 U.S. embargo on vehicle sales to Cuba was instituted, all vehicle sales were restricted. That restriction was eased in the past decade. Some Chinese and South Korean vehicles have arrived, but the main supply of new vehicles and spare parts in Cuba came from Russia until that country collapsed.

New Jersey’s ICE vehicle sales ban is part of a broader effort by Murphy to push residents into the green economy he envisions they want. Or at least the green economy he says they should accept. Ms. Klinger’s interview focused on the pushback to this green vision that extends from EVs to stoves, furnaces, and water heaters. Anything using fossil fuels is, or soon will become, a target of the Murphy administration.

New Jersey is a loyal ‘blue state’ following the Biden administration’s marching orders. The justification for this green economy push was explained by Ms. Klinger. “I think what we are looking toward is the opportunity to build a market around these cleaner and greener technologies. The market is moving in a certain direction, and some people don’t like the directionality of that movement.” Maybe they remember the “if you like your health plan, you can keep your health plan” pledge of President Barack Obama when he was selling the Affordable Care Act, which turned out to be a lie, and labeled “Pants on Fire” by PolitiFact.

The Wall Street Journal pointed to a June Pew Research Center survey showing 50% of Americans oppose a 2035 ban on new ICE vehicle sales, up from 51% in April 2021. Such sentiment carries little weight in Trenton. EVs only account for about 4.5% of New Jersey registered cars, clearly insufficient for Murphy. Moreover, EV sales are slowing, and dealer inventories are piling up. New Jersey tries to help residents buy EVs by offering an additional $4,000 tax credit for purchasing one on top of the $7,500 subsidy from Uncle Sam. However, income restrictions on receiving these benefits reduce their value. That is why car websites suggest leasing as the least costly EV option.

What we found most interesting was the rationale behind this green economy push explained by Ms. Klinger. Her comments have received little attention. She told The Kilowatts: “’I think we can control what we can control. And everything that we have done out of the administration has been voluntary incentive-based — really just opening up additional choice to consumers who choose to adopt this technology and want to get a really considerable amount of money back in their pockets to do so right. Part of the opposition to this program sort of fails to recognize that this money is out there. And, if New Jersey residents don’t take advantage of it, if they don’t choose to make this this switch, then that’s money that’s lost.’”

Ah ha! Free money! If you don’t get to the trough, you will be the loser. What could go wrong with free money? Oh wait, it was the “free money” mentality that drove the mortgage crisis that nearly brought down the U.S. and world economies in 2008. The alchemy of transiting high-risk, expensive home mortgages into AAA-rated, low-coupon securities is what created the crisis. It only emerged when the low-credit borrowers suddenly couldn’t pay their mortgages, sending them into default, and causing the value of the securities they were supporting to collapse. Like tugging on a thread, the entire fabric of financial markets came unraveled.

The year-old Inflation Reduction Act, which even Biden regrets its name, was designed to kick-start the shift to a green economy. It included $369 billion in green energy subsidies from the federal till. However, economics firm Penn Wharton, investment banker Goldman Sachs, and others produced cost estimates ranging from $1.0-$1.4 trillion, or 3-4 times the official estimate. Such spending will only add to our deficits, boost federal debt, and increase interest expenses on that debt in the government’s budget. More inflation, higher taxes, or reduced government spending on other items will be the outcome, while there may be little impact on carbon emissions and climate change. Few people will be better off from this policy move.

Last Tuesday’s Duds For Offshore Wind

The problems upsetting the East Coast offshore wind market ‒ inflation, supply chain issues, and the rising cost of capital – were in last Tuesday’s Gulf of Mexico wind lease sale. The Biden administration had talked up the significance of this first Gulf sale only for it to be a resounding dud!

The government offered three offshore wind leases for bid – one near Lake Charles, Louisiana, and two off Galveston, Texas. Only the Louisiana lease was contested with two bidders. Germany’s RWE Renewables won the 102,480-acre lease by paying $5.6 million. That works out to $54.65 per acre, well below the bounty the government collected from its last sale in the New York Bight area. The 2022 sale raised nearly 800 times more money ($4.37 billion) than the Gulf sale in a 64-round bidding contest. The average price per acre paid in that sale was 160 times what RWE paid.

Only two bids were received for the LA lease and none for the two TX leases. LA has a mandatory offshore wind utility purchase requirement TX does not.

In reviewing our offshore wind sale records, the Gulf outcome is more comparable to the 2013 sale result for the two leases off Massachusetts than any other sale. In that sale, 164,000 acres were leased for $3.8 million, or $23 per acre. The price paid per megawatt of potential offshore wind power was nearly $30,000/MW, nine times the price for the Louisiana lease.

BOEM Director Elizabeth Klein applauded the sale. “Today’s lease sale represents an important milestone for the Gulf of Mexico region — and for our nation — to transition to a clean energy future.” A more sobering view was offered by Mona Dajani, global head of renewables, energy and infrastructure at law firm Shearman and Sterling. “This first-ever Gulf offshore wind auction was viewed as a big deal, a potential game changer. Those of us hoping to see a real offshore wind boom in the Gulf may have to wait.”

And maybe wait for a long time. Why? Estimated Gulf wind speeds are lower than on the East or West Coasts. The Gulf’s gumbo seafloor may inflate the cost of installing wind turbines. Then there are hurricanes, something European wind turbines do not experience, so we have little knowledge of how they will stand up to a Category 3 or 4 storm.

The reason for the Louisiana lease with its 1.7 gigawatts (GW) of potential power was because the state has a mandate that local utilities buy 5 GW of offshore wind power by 2035. Texas does not have such a mandate.

The East Coast offshore wind industry is driven by state mandates. They grant monopoly power to offshore wind developers in selling their output – something no oil and gas company receives when it wins an offshore lease. They have to hope their research enables them to find and develop sufficient hydrocarbons to earn a profit, but they have no monopoly price power.

Will Louisiana utilities balk at the price for the offshore wind they must buy? This issue is what has the East Coast offshore wind industry in disarray as contracted power price agreements provide insufficient revenues for financing the projects. Estimates are that the Gulf’s offshore power price may be twice the cost of a natural gas plant. But mandates alter the level playing field of power prices. Will Louisianans be okay with rising electricity bills due to offshore wind?

That same day, Danish offshore wind developer, Ørsted, announced it would need to impair the value of its U.S. projects by up to Danish Kroner (DKr) 16 billion ($2.3 billion). Ørsted CEO Mads Nipper blamed supplier delays for potentially DKr 5 billion ($0.7 billion) of that total, higher interest rates for DKr 5 billion ($0.7 billion), and lower than expected U.S. investment tax credits for DKr 6 billion ($0.9 billion). The company’s share price dropped by nearly 25% the following day.

Virtually every East Coast offshore wind project not already under construction is facing similar cost pressures, which is why the developers are canceling their power purchase agreements and working to rebid their projects in upcoming offshore wind solicitations hoping for higher prices.

This is not the first impairment charge Ørsted has suffered. Last year it was forced to reduce the value of its New York Sunrise Wind project by DKr 2.5 billion ($0.4 billion) because of cost pressures. Ørsted is also facing cost pressures and inadequate subsidy issues in the U.K. and faces a decision about a major project. This comes after Sweden’s Vattenfall suspended work on its 1.4 GW Norfolk Boreas project because the government’s subsidy doesn’t cover the rapid increase in construction costs. It is the first of the company’s three wind farms in U.K. waters representing an investment of about £10-£11 billion ($13-$14 billion). Given that Ørsted’s Hornsea Three wind farm has the same level of subsidized electricity prices as Vattenfall’s should investors be prepared for another impairment charge?

Last Tuesday was not a good day for the U.S. offshore wind industry and one of its leading players. What are the implications for the pace of the industry and meeting the Biden administration’s target of installing 30 GW of offshore wind by 2030?

August Market Doldrums Are Over And Energy Did Well

The ‘dog days of summer’ describe August on Wall Street. People are on vacation. Trading volumes are low. News and trader actions can have a disproportionate impact on share prices. The business media struggles to explain the market’s daily ups and downs because they can’t just say: It’s August and this is what the market does!

Investors, traders, business reporters, and company executives struggle to divine what is happening in the economy and what trends will be important in the final third of the year. Moreover, they wrestle with what the global economy will be like in 2024 because it is time to put earnings forecasts together. With politicians back in their home districts, the news flow out of Washington is usually quiet, save for event-driven news, which this year was very active.

The S&P 500 Stock Index closed August with a small loss (-1.6%). Only one industry sector posted a gain for the month – Energy (1.8%). This marked the second consecutive month Energy was the top-performing sector. At the end of the first six months of 2023, we wrote that energy fundamentals seemed to be setting up for a better second half for the sector after a dismal first half. Oil prices began to rally, although oil and energy stocks remained an unpopular investment option for many professional traders and investors. Investors who rode Energy’s outperformance in 2022 remained steadfast optimists. But they endured periods of brutal oil price drops and accompanying poor performance for energy stocks. Their perseverance seems to be beginning to be rewarded.

Study the sector performance chart for 2022 and 2023 by focusing on the green squares. For most of 2022, the green squares are to the left (best-performing sectors), but they then moved to the far right (worst performers) when the calendar switched to 2024. In the past, we have seen Energy go from best to worst and back to the best-performing sector, and it looks like it is happening again.

Energy is the best-performing sector for August giving it two consecutive months as the top sector. Oil prices are breaking through resistance that could drive Energy higher during the rest of 2023.

WTI prices closed higher over August. The Saudi Arabia/Russia production cuts, augmented by additional export volume reductions, have tightened the crude oil market and elevated product prices. World economies continue to struggle but most are showing growth. Even with China’s economy stressed, global oil demand has reached a new high. Further demand growth, even with additional supply, will keep the world oil market tight and oil prices elevated. High oil prices drive energy company earnings and stock prices.

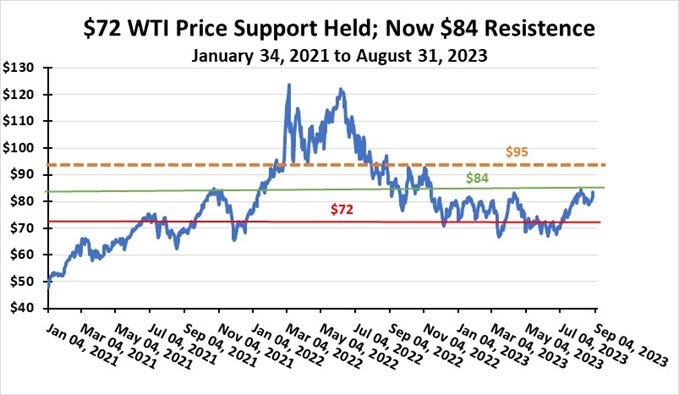

We have pointed out how $72 had been a support level for oil prices. That level held in July, and with oil prices continuing to rise, the question became where was resistance? It seemed to be about $84, and when prices reached that level, they fell. They are now knocking on that resistance door again. A break above that level would leave oil prices targeting the mid-$90s as the next resistance level. Breaking that barrier would leave an open field allowing oil prices to climb toward $100 or higher. We caution that these price moves can take months to unfold, with ups and downs along the way.

Oil prices have been trading in a tight range, but they are poised to break above current resistance that could send them even higher in the fourth quarter.

Energy may continue to be among the top-performing sectors for the balance of 2023. Although some investors also expect it to outperform in 2024, we will wait until we have more information about the economy and the oil demand/supply outlook. Geopolitical developments are always a wildcard. Given all the political drama unfolding in this country involving the former and current presidents, no one knows what might happen next year.