Energy Musings - January 27, 2025

Ørsted absorbed another impairment to its U.S. offshore wind assets with a painful outcome for shareholders. Why can't management avoid such financial disasters?

Ørsted Struggles With U.S. Offshore Wind Business

Last Monday, Danish wind developer Ørsted announced a series of impairment charges to its 2024 earnings due to problems with its U.S. offshore wind projects. This is the third time in the past 18 months that Ørsted management was forced to explain their business model failures. The impairments wiped out DKK 40.5 billion ($5.7 billion) of the company’s asset value. The stock price has fallen by nearly 54%, significantly hurting shareholders.

The latest impairment was DKK 12.1 billion ($1.7 billion) due to higher interest rates ($600 million), reduced book value of seabed leases ($500 million), and higher project costs for Sunrise Wind ($600 million). Management has used the same rationales to explain the prior impairments. One wonders how many more times impairments will blindside shareholders.

Management continues pointing to these issues as problems navigating the nascent U.S. offshore wind market. However, Ørsted has a history of success in other developing offshore wind markets. What makes the U.S. market so difficult? Maybe because management thought the days of low inflation and interest rates were the norm rather than the exception. Failing to consider alternative economic environments points to a weakness in the management of the business.

In August 2023, Ørsted surprised investors by announcing DKK 16 billion ($2.25 billion) of impairments. They were related to supply chain problems, the lack of progress in discussions with federal authorities about receiving the 10% incremental U.S. Investment Tax Credit, and higher long-dated U.S. interest rates. The charges were unsurprising to investors since other offshore wind developers had signaled they were experiencing cost problems, making projects unfinanceable because of the low electricity prices contracted.

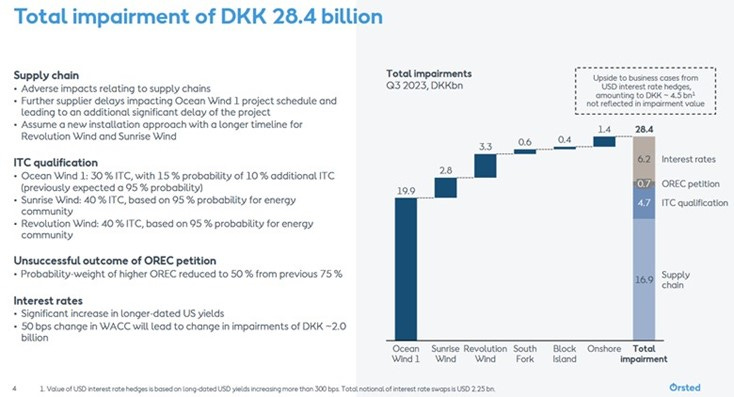

By October 2023, when Ørsted finally reported its third-quarter earnings, the impairment charge had swelled to DKK 28.4 billion ($3.99 billion). In the investor and analyst earnings presentation, the company showed a chart enumerating the components of the impairment charge. The impairment assigned to each of Ørsted’s offshore wind projects was shown. The chart also detailed the impairment by component – interest rates, reduced probability of higher Offshore Renewable Energy Certificate (prices), incremental ITC probabilities, and supply chain problems.

The Ocean Wind 1 project, located 15 miles off the coast of Atlantic City, New Jersey, accounted for 70% of the impairment charge. Eventually, the Ocean Wind 1 and 2 (1,100 and 1,148 megawatts (MW), respectively) projects were abandoned. That decision was included in Ørsted’s third-quarter earnings report. In the press release, David Hardy, Group EVP and CEO Americas, stated, “Macroeconomic factors have changed dramatically over a short period of time, with high inflation, rising interest rates, and supply chain bottlenecks impacting our long-term capital investments.”

The 2023 impairment charge crystallized problems of offshore wind.

When Ørsted reported its impairments in August 2023, it listed rising interest rates as impacting its asset value by up to DKK 5 billion ($700 million). When the company reported third-quarter earnings, the interest rate impact increased to DKK 6.2 billion ($870 million). Higher interest rates and supply chain problems were popular explanations by offshore wind developers for their project problems in 2023.

Ørsted showed in its 2023 annual report presentation in February 2024 how it matched 95% of its costs for operating and under-construction projects with long-term fixed debt. For projects awarded but not under construction, only 25% of the anticipated construction cost was matched with interest rate swaps, effectively locking in the projects’ cost and reducing exposure to volatile interest rates.

In 2023, developers of four offshore wind projects previously contracted by New York, including one of Ørsted’s, requested rate relief. They needed higher electricity prices to continue with the projects. The developers told New York utility regulators that they would cancel the projects without rate relief, even if it meant paying penalties. Offshore wind projects for Massachusetts and Connecticut had already been canceled, with developers paying penalties after being assured they could rebid their projects in future state solicitations.

New York not only agreed to allow developers to rebid their projects but also eliminated penalties for cancellations. This action was deliberate because New York could not meet its mandate for 70% of the state’s electricity to come from renewable energy by 2035.

Developers requested rate increases averaging 48% to advance the New York projects. Ørsted asked for the smallest increase – 27% ‒ for its Sunrise Wind project, a 992-megawatt (MW) wind farm off the tip of Long Island. The proposed Sunrise increase was from $110.37 per megawatt-hour (MWh) to $139.99.

Sunrise Wind is off Long Island and Massachusetts.

Sunrise Wind has been a challenging project for Ørsted, as the repeated impairments show. The company has tried to manage risks related to delays and costs for the fabrication and supply of monopile foundations by adding an additional supplier and extending installation vessel charters.

Installation vessels have become a significant problem for developers because of the Jones Act’s limitations. Ørsted contracted to use Dominion Energy’s Jones Act-compliant Charybdis vessel. Its delayed delivery meant it could not install turbines at the Revolution Wind and Sunrise Wind projects as scheduled. Ørsted switched to an alternative system that relies on a Jones Act-compliant barge that brings components to a foreign-flag installation vessel. This system is less efficient, according to Ørsted, meaning higher costs.

Based on the company’s experience with the installation progress of Revolution Wind, management adjusted the Sunrise Wind construction plan. It will now extend over two winter installation windows. Based on the installation experience at Revolution Wind, the company has reduced the anticipated turbine installation rate at Sunrise Wind. This has pushed out the commissioning of Sunrise to 2027 from 2026 and added to the project’s cost.

Ørsted also experienced problems with the equipment fabrication, installation, and commissioning of the first-ever U.S. offshore high-voltage direct current power system. The design and fabrication of the platform caused delays. The export power cable was also found to have defects, requiring that it be redesigned and remanufactured. The combination of these problems led to increased vessel costs. The ultimate problem is that the cost increases wiped out the project’s financial contingencies, forcing management to add more money to the project.

Management says the Sunrise Wind project remains profitable with a mid-single-digit lifecycle internal rate of return. Does this calculation include the federal production tax credit or investment tax credit? The Inflation Reduction Act extended the life of these subsidies until the U.S. reduces its emissions to 25% of 2022 levels, a target likely never to be met before 2050. This ensures that the production tax credit can last 25 years or longer. That ensured income stream may justify accepting IRRs of 5% for multi-billion dollar investments.

An offshore wind project can receive 2.6 cents per kilowatt-hour or a full investment tax credit of 30%. An additional 10% ITC can be added to the 30% by meeting domestic content thresholds and/or locating facilities in fossil-fuel-dependent “energy communities.”

The latest challenge for Ørsted will be navigating the shifting regulatory landscape under President Trump’s offshore wind leasing and permit approval process. Developers believe that with permits and approvals, they can continue constructing their offshore wind farms. However, the new administration has ordered a comprehensive environmental study of the impact of offshore wind farms on the Atlantic Ocean. We do not know if the Bureau of Ocean Energy Management (BOEM) has offered developers waivers to complete wind farm environmental studies as it does for posting decommissioning bonds. Therefore, it is possible some of these projects could experience other delays.

The offshore wind industry will be in turmoil for quite a while. Its turmoil will create problems for the states depending on offshore wind to meet their clean energy mandates. This turmoil comes as the electric utility industry begins to wrestle with meeting accelerating power demand and complying with clean energy mandates. Nuclear energy may be the ultimate beneficiary of offshore wind’s turmoil.