Energy Musings - February 2, 2024

We provide our monthly report on Energy and sector stock market performance for January and discuss influencing factors. In response to a question, we have updated the ESG flows information.

Energy Stocks Suffered In January But World Isn’t Ending

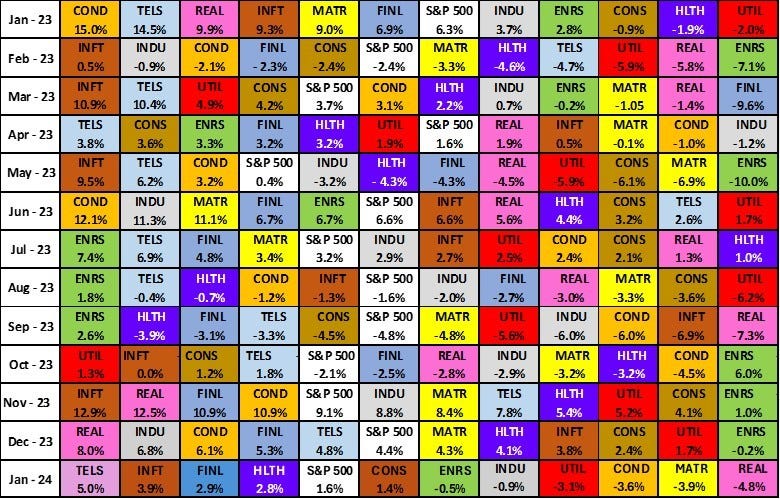

January saw the Energy sector of the Standard & Poor’s 500 Index suffer a small loss (-0.5%) for the month. While a performance disappointment, the sector finished exactly in the middle of the 11 sectors. That was a nice position, given Energy finishing last for each of October, November, and December, something it had not done in years.

The stock market continued its rally that started midway through the fourth quarter when investor sentiment embraced the scenario that the Federal Reserve was done hiking interest rates to tame inflation and would begin a serious rate-cutting phase in 2024. The odds were high that the Fed would make its first rate cut in March. The prospect of lower interest rates coupled with reduced inflation would boost the earnings of financial institutions along with improving the economic outlook for stocks sensitive to interest rates such as utilities. Reduced interest rates are also bullish for stock market valuations of companies which was helpful for technology stocks that drove the market’s performance in 2023 and continued in January 2024.

The bullishness evaporated last Wednesday when the Federal Reserve finished its latest two-day meeting and announced it was holding the fed funds rate steady. More damagingly, Chairman Jerome Powell took a somewhat hawkish tone in his afternoon press conference by suggesting that a March rate cut was not the focus of the Fed members. The stock market suffered a large decline as a result.

Energy stocks lost a small amount during January but finished in the middle of the pack of S&P 500 sectors.

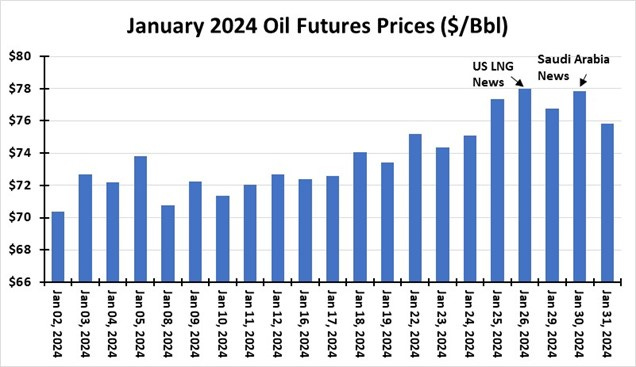

Energy’s performance was hurt by a decline in oil prices at the end of the month, driven by negative industry news, the easing of geopolitical tensions in the Middle East, warmer weather that reversed production cuts caused by the earlier polar vortex, and a market sentiment shift. The following chart shows the daily oil futures price for January. While there was routine volatility, oil prices steadily rose throughout the month reaching a peak on Friday, January 26. Even after the final day’s decline, oil still rose nearly 6% during the month. It was the first positive month for oil prices since September 2023.

Oil prices posted a nearly 6% increase in January for the first positive month since last September.

On January 26, the White House announced it was going to pause the approval process for new liquefied natural gas export terminals. The pause was to allow the regulators to update their models for the impact of gas exports on climate change, U.S. energy markets, and inflation. The reality was that it was a blatant attempt by the Biden administration to buy Gen Zer’s votes in the upcoming presidential election. This age group is reportedly highly fearful of the damage to the environment, economy, and mental health from climate change.

While not directly related to oil, the White House announcement reminded investors of the government’s ongoing efforts to damage the domestic energy industry. Those concerns were ramped up sharply when Aramco, Saudi Arabia’s national oil company, announced it had received direction from the government to not increase its productive capacity from 12 to 13 million barrels per day. The initial interpretation was that Saudi Arabia was worried about global oil demand growth. That certainly fits with the climate change narrative that we are near or at peak oil demand.

The reality, however, is that the Saudi Arabian government believes the money could be better spent on other economic initiatives that were in its Vision 2030 priorities, especially some included in the Kingdom’s green initiatives that were delayed last year. Aramco and Saudi Arabia have accessed the debt market in recent years. Therefore, the recent spending decision could be reversed or financed from debt offerings, so it is dangerous to attribute the government’s order to Aramco as a statement about future oil demand. Lastly, a key goal of Saudi Arabia’s domestic energy efficiency and renewable energy push is to free up one million barrels a day of current crude oil output for export rather than to generate power and operate desalination facilities.

What we know is that traders and algorithms react to initial news reports and believe the simplest explanation. Sell first and analyze later is their strategy. Shares can always be repurchased if the analysis confirms the decision to be wrong.

Energy remained under pressure in the early February trading as crude oil prices continued to slide. February is known to be one of the worst months for stock market performance. We wonder if it will be true this year. Punxsutawney Phil saw did not see his shadow Friday morning. An early spring means less heating oil demand particularly in the Northeast, which means less oil use. However, an early spring may bring the driving season forward which can boost gasoline consumption. We will be watching as February unfolds.

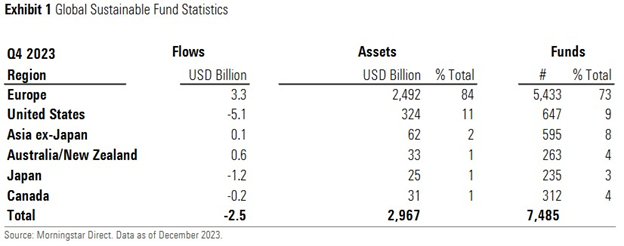

ESG Investment Flows Update

Our February 1st Energy Musings article dealt with the flow of funds in and out of ESG funds in Europe, the United States, and Japan. We neglected to discuss the relative significance of those flows, as we were focused on the fact that European ESG funds experienced a $3.3 billion net inflow despite serious pushback from citizens against government green energy agendas. Both the U.S. and Japan experienced net outflows from ESG funds.

As the chart below shows, Europe dominates the ESG investing business. Its $3.3 billion net inflow represents only 0.1% of total ESG assets, making the gain insignificant. U.S. and Japanese net outflows were more significant as they represented 1.6% and 4.8% losses, respectively. It will be interesting to watch ESG investment flows during 2024.

The $3.3 billion net inflow to European ESG funds was negligible to total assets - outflows were more significant.