Energy Musings - February 10, 2025

European oil companies are struggling with low share valuations because of their green energy focus. Companies are abandoning them and taking other shareholder friendly actions.

Europe’s Oil Companies Struggle For Investor Attention

European oil companies are suddenly correcting course as they struggle to win back investor interest. , Shifts started as much as two years ago or recently, depending on the company. Two shifts involved installing new CEOs to lead new strategies. Two others are making strategy adjustments to win investor backing. In each case, the board of directors understood that their company’s strategy needed to change to boost earnings, share price, and investor returns.

In February, Equinor, the Norwegian state-backed energy group formerly Statoil, told investors it was planning to increase fossil fuel production and halve its spending on renewables. New targets included boosting oil and gas output to 2.2 million barrels by 2030, a 10% increase. Equinor is also cutting its renewable generation target to 10-12 gigawatts (GW) from 12-16 GW. Renewable and low-carbon technology spending for 2025-2027 would be halved to $5 billion. The company offset some of its renewables spending cuts by buying nearly 10% of Danish wind developer Ørsted last October. However, their investment is underwater by roughly a third, given Ørsted’s operational woes, impairment charges, and management change.

CEO Andres Opedal said Equinor would generate more free cash flow “by high-grading the portfolio, reducing the investment outlook for renewables and low-carbon solution, and improving cost across our organization.” He concluded, “By adapting to [the] market situation and opportunities, we are set to create shareholder value for decades to come.”

Vitol, the world’s largest independent energy trader, outlined the reality of the global oil market. It said world oil demand would not decline before 2040. Their forecast aligns with those of ExxonMobil, Chevron, and other major U.S. oil companies.

The most recent European oil company to announce a strategy shift was TotalEnergies, headquartered in Paris, France. The company announced it would convert its American Depositary Receipts (ADRs) into listed shares on the New York Stock Exchange. The move should improve share liquidity and attract more U.S. investors.

The ADR move does not constitute a dual listing, as Paris will remain the company’s headquarters and primary market for new shares. Once the legal details are finalized, the Paris and New York-listed shares will be transferable from one market to another and share prices will correlate to the closest exchange rate.

TotalEnergies also announced it was targeting buying back $2 billion worth of shares each quarter in 2025. This is a cost-effective and popular way to return capital to shareholders.

The move by TotalEnergies is the latest action by a European oil company to try to close the valuation gap with its U.S.-based oil company competitors. Europe’s green energy focus has caused European money managers and investors to shun the shares of their local oil companies. The green focus caused oil companies to stop investing in their core, profitable business in favor of less profitable renewables. Former BP plc CEO Bernard Looney, after becoming CEO in 2022, warned shareholders that the company’s earnings and dividends might not grow as they had in the past. That reality angered BP pensioners who depended on increasing dividends.

Shell plc became noteworthy when it reported earnings at the end of January. The company’s earnings were hit with a $1 billion impairment charge for acting on its new business strategy. The strategy shifted after installing Wael Sawan as CEO in January 2023. The 25-year-old chemical engineer Shell veteran oversaw its integrated gas and renewables division before being elevated to head the company. Months after evaluating Shell’s strategy, Sawan announced Shell would drop its plan to cut oil production each year for the rest of the decade. Shell’s power business would focus on select markets and segments while exiting others.

Sawan and Shell’s Board of Directors investigated shifting its incorporation and share-listing to the United States. Recently, Sawan said the move was not a top priority but remained a discussion topic.

Sawan has made the case that many renewable investments, particularly offshore wind, were poor uses of Shell’s capital and talent. His conclusions are based on his experience overseeing Shell’s renewables business. To that end, Shell withdrew from Southcoast Wind and, recently, the Atlantic Shores offshore wind projects. The latest move contributed to New Jersey killing further offshore wind development plans.

Patrick Pouyanné, TotalEnergies CEO, said it was “not worth” pursuing U.S. offshore wind projects while President Donald Trump is in office. He gave offshore wind projects “little chance of being authorized” because Trump opposed them. As almost every U.S. offshore wind project is being done by European oil companies, that is another weight on their share prices.

BP plc is the latest European oil company to come under investor scrutiny. A Reuters story was titled “BP now stands for ‘Best Partitioned.’” It was a play on BP’s turn of the century Beyond Petroleum when then-CEO John Browne directed the company into lower-carbon energy.

After Looney was ousted as CEO, BP’s board selected the company’s former CFO Murray Auchincloss to head it up. Looney’s push into green energy, warning investors the move could be costly, proved unpopular with them. Auchincloss is moving to address costs and strategy. He has announced layoffs and asset sales, but needs to do more to boost BP’s standing among its peers.

Like other European oil companies, Auchincloss rolled back Looney’s planned hydrocarbon production cuts. Future production might be lower if BP sells more assets to address its massive debt load. BP’s net debt, including leases, is 31% of capital employed. HSBC analysts expect BP’s leverage to remain the highest until 2030 among the five major oil companies they monitor. This leverage prevents BP from shoveling cash to investors to win their support.

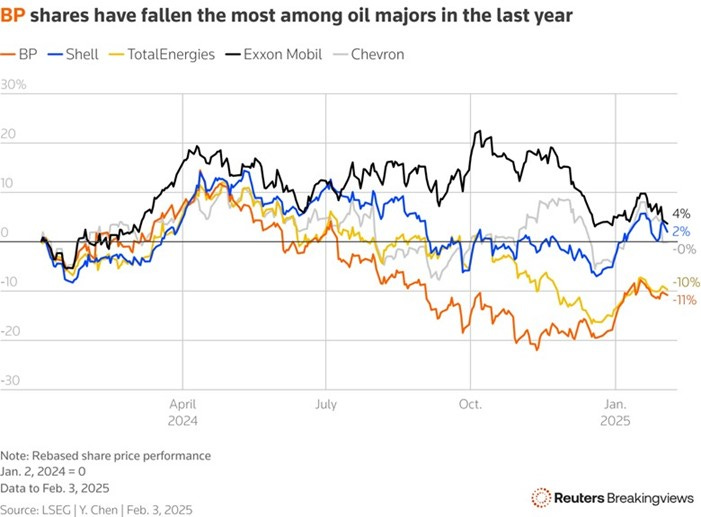

BP shares woefully underperformed for most of 2024.

BP’s share performance since January 2, 2024, shows how shareholders have suffered. BP’s share price fell 11%, slightly worse than Paris rival TotalEnergies, but woefully underperforming ExxonMobil, Chevron, and, importantly, London-based competitor Shell.

A Reuters investment analyst speculates that BP’s valuation metrics make it a perfect candidate for a corporate breakup, thus the title of her report. BP trades three times its estimated 2025 earnings before interest, taxes, depreciation, and amortization (EBITDA). That is lower than Shell’s four times and ExxonMobil’s seven times.

While noting BP’s low valuation, Reuters lays out a case for why Auchincloss might look at breaking up the company and selling operations. The breakup strategy is in the limelight as industrial giant Honeywell announced it is exploring splitting into three units, similar to General Electric’s successful move several years ago.

Various analyst reports show BP’s business units, net of its debt, total nearly 60% more than its current market value. This is always a tempting analysis, usually done by value investors seeking investments worth much more than their current market worth in hopes investment sentiment will shift and the value gap closes.

There have been numerous mergers and acquisitions in the oil patch in recent years. Those deals allowed the acquirer to secure strategic assets to fill out their portfolios. BP has often been included in those analyses, but no deal has yet emerged.

By backing away from the green-energy focus, BP hopes investors recognize the company is undervalued. BP is likely watching TotalEnergies’ share price after its announcement to list its ADRs and make them equivalent to its Paris shares. A sustained positive investor response may give BP another restructuring option. Mainly, BP has to hope European governments’ retreat from their green energy push will spur European investors to re-invest in local oil and gas shares.

The latest BP news came on Saturday when Bloomberg.com exclusively reported that activist investor Elliott Investment Management had accumulated an unknown stake in BP. Elliott sees BP shares as undervalued and will be urging management to act to close the valuation gap with its peers. BP is worth half the value of Shell. This development is consistent with our previous comments on the strategy challenge facing BP management and the company’s attraction for value investors.

At the end of February, BP management will provide a strategic update. Bloomberg says BP will announce “a clearer shift back toward oil and gas,” consistent with the moves of Shell and TotalEnergies. The announcement of cutting 5% of its labor force (4,700 jobs) and eliminating 3,000 contractor positions are likely insufficient for Elliott and will do little to close BP’s market value gap.

Stay tuned. We could be watching the end of BP’s glorious and sometimes infamous history.